Retirement planning comes with big decisions — choosing your retirement date, filing forms, and mapping out your income. Plus, CalPERS has its own lingo to describe the process.

To make things easier, we’ve rounded up key terms and resources to help you confidently plan your next chapter.

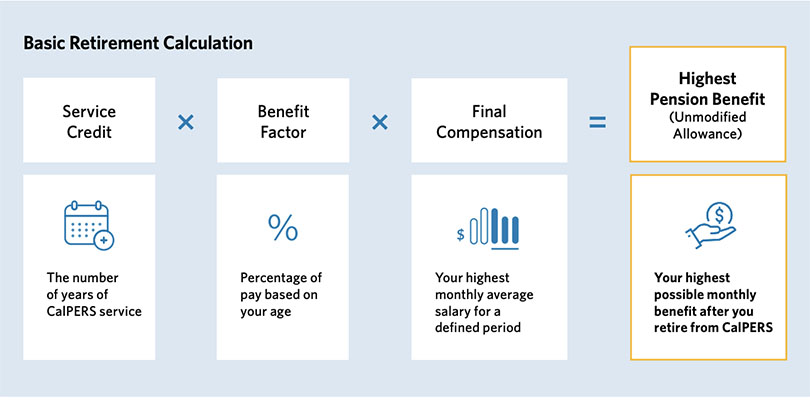

Benefit Factor

Your benefit factor is the percentage of pay you earn for each year of CalPERS-covered service. Along with your total service credit and final compensation, it’s a key piece in calculating your pension.

For a detailed breakdown of benefit factors by retirement age and years of service, check out our Benefit Factor Charts.

Our Planning Your Service Retirement (PDF) guide offers a clear look at how your benefit factor impacts your final pension amount.

Classic vs. PEPRA Member

If you were hired and enrolled in CalPERS before January 1, 2013, you’re considered a classic member. This means you were hired before pension reform rules went into place.

You are considered a Public Employees’ Pension Reform Act (PEPRA) member if you joined CalPERS for the first time on or after January 1, 2013, and meet the following criteria:

- You had no prior membership in another public retirement system.

- You were a member of another public retirement system but were ineligible for reciprocity.

PEPRA members in particular are encouraged to take advantage of supplemental income plans, such as 401(k) and 457 savings plans through Savings Plus, or the CalPERS 457 plan.

Learn more in our article, PEPRA Members: How to Boost Your Retirement Income, or in our video on the Public Employees’ Pension Reform Act (PEPRA).

Cost-of-Living Adjustment (COLA)

The cost-of-living adjustment (COLA) increases retirement benefits for retirees, survivors, and beneficiaries, helping your payments keep pace with inflation. You’ll receive your first COLA in the second calendar year after your retirement date, with the adjustment paid during the May 1 warrant period.

To shorten the wait for your first COLA, consider carefully the specific date you choose to retire. Learn more about the power of compounding growth in our article, COLA’s Secret to Retirement Security, and in our video How COLA and Compounding Work Together to Boost Your Retirement.

Community Property

In California, anything you earn or acquire during your marriage or registered domestic partnership—including money, retirement benefits, property, and assets—belongs equally to both partners. These assets are considered community property. If the relationship ends in divorce or legal separation, these assets, including your retirement benefits, may be divided between you.

Learn more in our article, Divorce, Your Pension, and Community Property: Simple but Not Easy, and in our Guide to CalPERS Community Property (PDF).

Defined Benefit Plan

The CalPERS defined benefit plan is the main retirement option for California public employees, including state, school, and many local government workers. With a defined benefit plan, you receive lifetime pension payments that are calculated using a set formula.

In contrast, defined contribution plans—like a 401(k) or 457 plans—depend entirely on how much money you and your employer contribute, plus any investment earnings.

Disability Retirement

If you have a disabling injury or illness that prevents you from working, you may qualify for disability retirement. Unlike regular service retirement, there’s no minimum age requirement, and your disability doesn’t have to be job-related. To be eligible, you generally need at least five years of service credit, though there are some exceptions.

Learn more in A Guide to Completing Your CalPERS Disability Retirement Election Application (PDF).

Final Compensation

Final compensation is one of the three key factors used to calculate your pension—not to be confused with your total pension amount. It refers to the highest average annual pay you earned during any consecutive 12- or 36-month period of your employment.

We use your full-time pay rate—not your actual earnings—to calculate your final compensation. If you work part-time, we use your full-time equivalent pay rate for this calculation.

For more details on how your final compensation is calculated, take a look at our Planning Your Service Retirement (PDF) guide.

Power of Attorney

Designating a CalPERS special power of attorney (POA) ensures someone you trust can manage your retirement benefits if you become incapacitated and/or unable to do so yourself. Without a designated POA, important decisions—like updating your information, changing tax withholdings, or making benefit elections—could be delayed or handled by someone who may not know your wishes.

Learn more in our article, Secure Your Retirement: Assign a CalPERS Power of Attorney Today, and in A Guide to Your CalPERS Special Power of Attorney (PDF).

Reciprocity, Or Moving Between Retirement Systems

Reciprocity lets you transfer between different public retirement systems in California without losing your benefits. CalPERS has agreements with many other public retirement systems, so you can move from one public employer to another—within a specified time frame—and keep your retirement rights.

When you use reciprocity, you become a member of both systems. You’ll need to retire from each system separately and will receive separate retirement checks from each.

Learn more in our article, What You Need to Know About Reciprocity, and our publication on When You Change Retirement Systems (PDF).

Service Credit

Service credit is the number of years you’ve worked for a CalPERS employer. It’s one of three factors—along with your final compensation amount and benefit formula—that determine the size of your monthly pension check.

In some cases, you can purchase service credit and improve your total pension amount. Learn more in our article, Service Credit Secrets: Your Key to Maximizing Benefits, and see how your CalPERS pension is influenced by your service credit in this short video.

Service Retirement

You can apply for service retirement when you’ve worked enough years and reached the required age to receive your retirement benefits.

Check out our retirement planning checklist for tips to help you prepare as you get closer to your well-earned retirement. Learn more in our article, Tips to Get the Most Out of Your Retirement Benefits, read about service retirement frequently asked questions (PDF), or check out our Planning Your Service Retirement (PDF) publication.

Survivor Continuance

Survivor continuance is a monthly benefit, paid by your employer, that goes to an eligible family member after your death in retirement. The law determines who qualifies as your survivor, so you cannot choose this person yourself.

Survivor continuance is automatically provided by law to all state and school members. However, public agency employers must contract with CalPERS to offer this benefit. To qualify, you must have an eligible survivor at the time you retire, and that person must remain eligible until your death.

Learn more about the survivor continuance monthly benefit in Post-Retirement Survivor Benefits: For Retired Members (PDF).

Temporary Annuity

A temporary annuity allows you to adjust your monthly service pension payment on the front-end. At retirement, you can choose to receive a temporary annuity, which adds an extra amount to your monthly CalPERS pension check for a set period of time.

You can think of this annuity as an “advance” on your future monthly payments, which can help cover higher expenses or specific needs in the early years of retirement. After the temporary annuity period ends, your monthly pension payments will be permanently reduced.

For more details on selecting and calculating yours, check out our Guide to Your CalPERS Temporary Annuity (PDF).

Unmodified Allowance

Receiving the highest possible pension payment at retirement is called your unmodified allowance. This option provides you with a monthly benefit that stops when you pass away, unless you’ve made any modifications. If you choose the unmodified allowance, you cannot name a beneficiary, so no benefits will be paid to anyone after your death.

Learn more in our article, Curious About CalPERS Retirement Payment Options?